[ad_1]

Greetings from Missouri. This has been a few “at dwelling” weeks previous to a travel-heavy February, which has allowed us to probe just a little deeper into fourth quarter earnings. For the reason that final Temporary, Jim’s interview with the 5G Guys podcast has been printed (right here and in addition a part of the opening pic). Many due to Dan McVaugh and Wayne Smith for being such gracious hosts.

As a result of Constitution has but to publish earnings (presently scheduled for Friday, February 2, previous to the market open), our market feedback can have extra of a give attention to AT&T, Verizon and T-Cell. We are going to cowl cable within the February 10th Temporary. Talking of cable, one correction to the earlier Temporary after talking with the corporate: We said “And, since Spectrum Cell’s (LTE) information is deprioritized relative to many premium Verizon plans (however higher than some supplied by Xfinity Cell – see Mild studying article right here), LTE can get very gradual (< 1 Mbps obtain speeds widespread in lots of KC northland places).” Seems that Verizon’s LTE obtain information speeds in north Kansas metropolis (and far of Missouri outdoors of the three largest metropolitan areas) is simply gradual and that the identical bit prioritization applies to each Spectrum Cell and Verizon’s premium plans (referred to as qci8). Our apologies to Constitution, and we will likely be happier Spectrum Cell prospects after Verizon completes their C-band upgrades all through the Metropolis of Fountains.

The fortnight that was

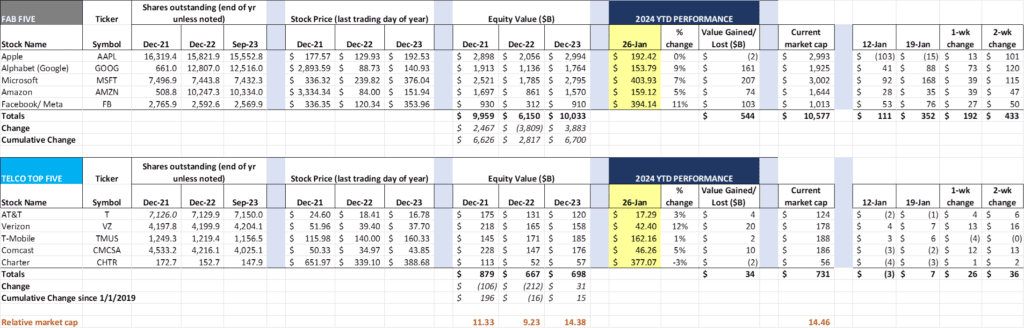

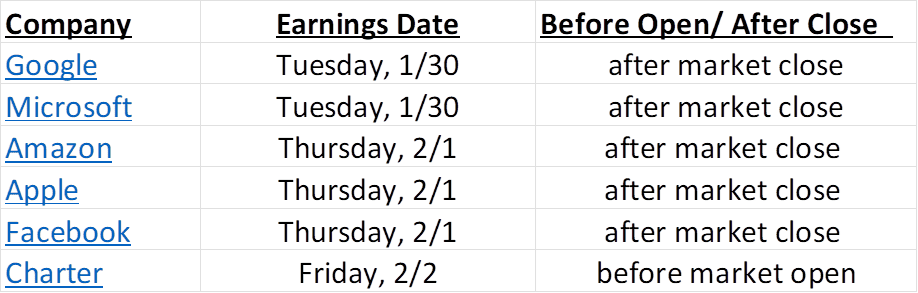

One other couple of weeks of “How good may it’s?” anticipation of Fab 5 earnings. In consequence, the group was up $111 billion this week and $352 billion over the fortnight. We expect that “fixed foreign money” will likely be a well-used time period on every convention name. In case you want the schedule, the remaining six convention calls of the ten shares that we cowl are listed under.

We will likely be fastidiously wanting on the development charges for every of the cloud suppliers (AWS/ Amazon, Microsoft, and Google). Additionally, Microsoft just isn’t possible to offer their Copilot early adoption statistics, however it received’t hold analysts from asking (and estimating). Our guess from discussions at CES and with a number of of you is that adoption goes to take some time and that $30/ seat/ mo. is a bit steep.

4 of the Telco High 5 reported final week, and every reporting firm noticed good points. T-Cell introduced that they now have 1.205 billion totally diluted shares as of the tip of the yr, which now contains the 48.752 million shares issued to Softbank because of reaching a trade-weighted inventory value above $150 for 45 consecutive days. T-Cell additionally had fewer inventory buybacks within the quarter, which they attributed to the unsure timing of the Softback share set off. The year-end share value figured will likely be up to date by the Feb 10 Temporary, and the present T-Cell market capitalization is ~ $194 billion as of Friday’s shut.

Due to the earnings evaluation under, we are going to hold this week’s market commentary brief, leaving time for celebration of the Apple Macintosh’s 40th birthday. We learn many tributes to Apple’s longest-running product line, and suppose that Mashable’s is the very best (embedded in that article is one other web site referred to as https://mac40th.com/ which has lots of the previous ads – undoubtedly a visit down reminiscence lane for Era X and earlier age teams).

Fourth quarter earnings—who has the momentum?

On this evaluation we take a look at Verizon, AT&T, and T-Cell 4Q 2023 earnings. Till Constitution studies, the straightforward reply to the query will likely be “possible T-Cell” however Constitution may shock to the upside, notably on wi-fi internet additions.

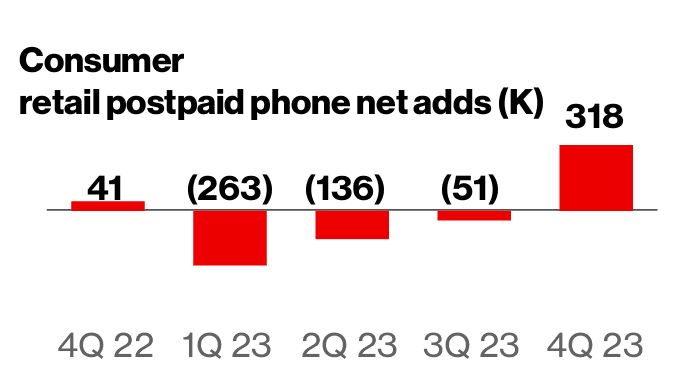

Verizon led off the earnings parade and created a number of pleasure over their wi-fi postpaid telephone gross additions determine (up 16.9% from 4Q 2022 to 2.3 million from 1.8 million in 3Q 2023). As we mentioned within the final Temporary, Large Crimson pulled a number of gross additions in to finish 2022. So the 17% development determine is much more outstanding. Close by is the online additions chart from their earnings presentation.

Plenty of that development is because of the myPlan value restructuring (Verizon’s CFO, Tony Skiadas, indicated within the 3Q convention name that 70% of the myPlan additions have been on their premium plan community tier). This could lead to incremental (gross add) ARPU development of about 5-9%, relying on which non-compulsory objects have been chosen (see right here for his or her present record, and in addition word that the Max + Netflix bundle was launched in December). We credited Verizon’s introduction of myPlan as one of many six key occasions in telecom in 2023 (Temporary right here) and suppose that it’ll proceed to be a key driver of incremental worth for the corporate.

However we don’t suppose that’s the one purpose why Verizon turned it round this quarter. Within the third quarter convention name, Michael Rollins of Citi requested a query about pay as you go to postpaid integration. Right here is Hans Vestberg’s response (transcript right here and emphasis and edit added):

“On the worth section in pay as you go and TracFone. As we mentioned within the ready remarks, we have been on the low level within the first half of ’23. And from right here on, we should always begin sequentially bettering. Secondly, that is actually vital for our technique. We wish to construct the community [adds] and have as many connections as attainable, and deal with the complete market on wi-fi. And naturally, being robust and being the #1 within the worth section is vital. Then from a market viewpoint, everyone knows that there was some kind of a mix between the low finish on postpaid and pay as you go, which implies that the volumes in pay as you go is just a little bit decrease. And we have now not been a part of that transformation of taking buyer for pay as you go. So what we’re doing proper now in our personal operation, which is loads, however one, we’re increase Whole by Verizon, which is a superb seed we have now on opening new doorways. That’s going to assist us to maneuver up the postpaid for the shoppers that wish to do this, but in addition have a high-end worth proposition. Secondly, we work with the nationwide retailers that we have now to see that we’re fortifying our choices in our retailer. And eventually, you’re seeing that DISH Seen continues with the tempo it has. After which we’re working with a number of different issues. So it’s a number of ongoing right here that provides us confidence that we are going to sequentially proceed to enhance. However clearly, this is essential for our total technique.” (edited and emphasis added)

As Hans and the crew headed into 4Q, pay as you go to postpaid conversion was on the mind. Our guess (and it’s solely that) is that they started to crack the code (if you happen to evaluate the myPlan to Whole Wi-fi plans right here, it might make sense to make the soar to postpaid with the precise credit score rating). They might have been doing it even sooner than the fourth quarter, as their 10-Q schedule (obtain right here) exhibits on web page 43. Or the offsets for each 3Q and the primary three quarters of the yr might be a coincidence. Clearly nevertheless, the chance to transform the best high quality pay as you go prospects to postpaid (notably telephone prospects) was on Verizon’s 4Q record.

Verizon had 21.4 million pay as you go subscribers on the finish of 3Q. Might an incremental 300-400K (1-2% of the bottom) have certified due to programs and course of work executed within the quarter? If that’s true (we wouldn’t rule it out), then there are many extra conversions coming. We expect there are as many as 4 million that they may convey into the postpaid fold as Seen and Whole by Verizon proceed to mature.

Merely transferring prospects from pay as you go to postpaid, nevertheless, doesn’t change the expansion in client service revenues. As was famous on the decision, service revenues have to develop. For 2023, Verizon grew whole wi-fi (enterprise and client) service revenues by $2.3 billion (3.2%), with 80%+ of that development coming from the Client enterprise unit.

Throughout the Client unit is the cable wholesale development. Cable has grown simply over 4 million internet subscribers over the 4 quarters from 4Q 2022 by 3Q 2023. This equates to roughly 33-34 million new month-to-month RGUs for the yr (this quantity might be understated as we aren’t fairly positive how effectively Cox carried out in 2023 however added in about 1 million incremental RGUs for them).

Per the working statistics within the Monetary and Working Data earnings complement, Client grew their service revenues by $1.85 billion in 2023. Of this quantity we estimate that not less than $550 million (30%) got here from the cable MVNO. Extra development got here from value will increase, mounted wi-fi development, and myPlan success, however, since there was no dialogue of the cable vector, we thought we would supply an estimate. (If we’re materially incorrect with the 30% determine, we might name into query why Verizon could be leaving cash on the desk as this per unit price displays a ~50% gross margin for the MVNO service revenues).

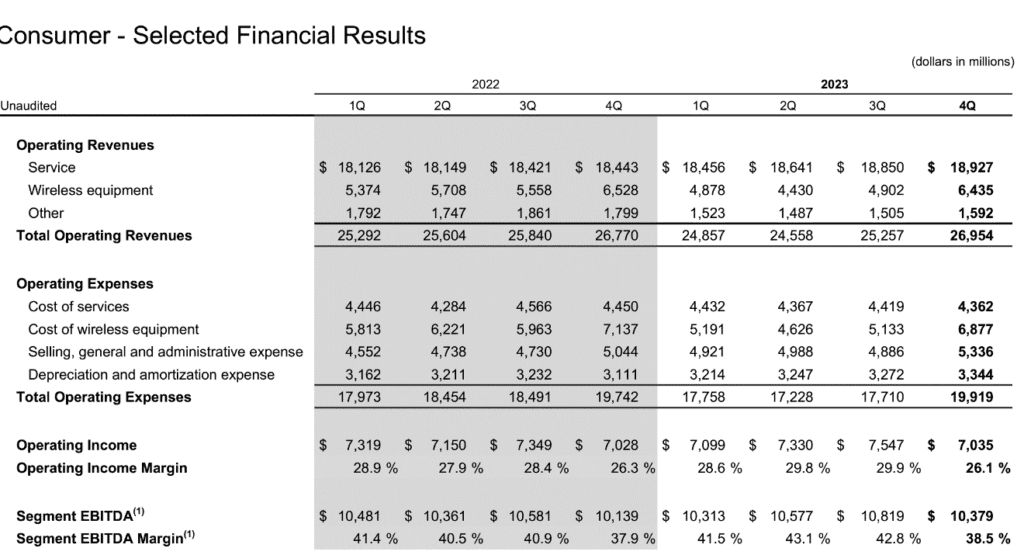

Being 30% of service income development is one factor, however right here is Verizon Client’s EBITDA image (word that the service income line for the complete enterprise unit contains each FiOS and wi-fi):

Phase EBITDA for Verizon’s Client unit grew a mere $526 million in 2023. Due to the excessive margins within the cable enterprise, it’s extremely possible that there could be very totally different EBITDA storylines with out cable’s contribution (which we predict is within the $450-475 million vary for 2023).

Backside line – Verizon: Verizon has myPlan momentum and is 1-2 additional adders away from runaway success (we predict a VPN addition like Norton could be extremely interesting, as would a revamped Google One or the power to buy a standing degree with Shell or Marriott or Nationwide or Uber). However among the income and many of the EBITDA momentum has to do with cable, and Verizon could be telling a really totally different story with out that foundational money circulate.

AT&T additionally had an excellent exhibiting and made progress on many fronts. It’s arduous, nevertheless, to disregard the huge debt load which locations a development albatross across the neck of the corporate. At present, the corporate has slightly below a 3.0 internet debt to adjusted EBITDA leverage ratio, and the corporate has pledged to convey that determine all the way down to 2.5x within the subsequent six quarters. This compares to a 2.6x internet unsecured internet debt leverage ratio for Verizon (3.1x when secured debt is taken into account) and a 2.5x ratio for T-Cell.

Assuming we have now an AT&T 2024 EBITDA development price that’s greater than 2023’s 4.7% determine (6% development to $46 billion which is 2x what was focused of their announcement), AT&T would want to decrease their whole debt to ~$115 billion to hit the two.5 determine (~$14 billion in debt discount). We expect it’ll be on its means by the tip of 2024 however is not going to try to overachieve this ratio till each the fiber and the C-Band applications are nearing completion. It’s possible that their ratio will likely be in ~2.7x vary by the point we take a look at 4Q 2024 outcomes. Evidently there’s a deleveraging focus on the firm that’s not current at T-Cell.

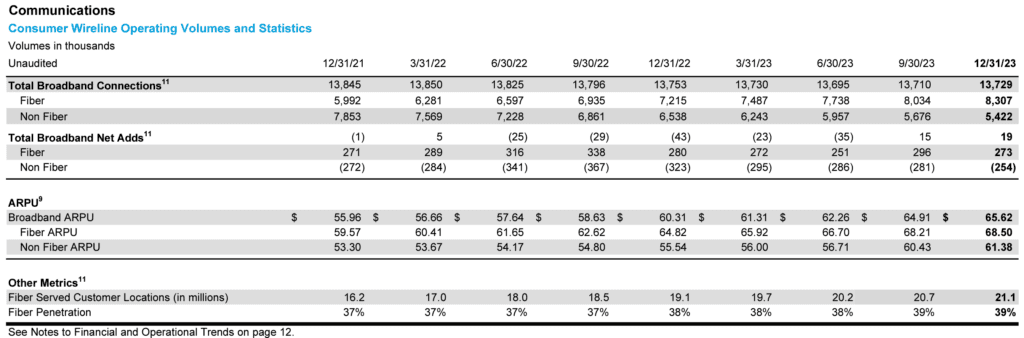

AT&T is transferring very aggressively to complete (and maybe develop) their fiber to the house program, and we noticed of their outcomes the fruits of three+ years of accelerated builds. Right here’s the chart from the monetary and working tables exhibiting the places and takes:

AT&T is in peril of lacking their purpose of constructing to 30 million places by the tip of 2025. The above determine exhibits 21.1 million houses handed with fiber and there are about 2.9-3.1 million companies that additionally contribute to the purpose. So that they stand at 24.0–24.2 million places handed with fiber and eight quarters to go. At their present tempo, they might come up about 2 million houses brief (500K client places per quarter for the subsequent 8 quarters). The corporate didn’t deal with their acceleration plan, however we count on extra colour on this in upcoming investor conferences.

Fiber internet additions development continues to be constructive (so higher than Comcast and we assume Constitution) however just isn’t accelerating. That is particularly attention-grabbing as a result of the second half of 2023 was when AT&T started to introduce cross-bundle reductions with wi-fi ($20/ mo. low cost from the fiber invoice if the shopper can be a wi-fi subscriber – extra right here). It looks like that ought to have been a needle mover on quantity, however actually solely slowed down the expansion of fiber ARPU development (nonetheless robust at 5.7% however down from 3Q’s 8.9%).

Within the subsequent Temporary we are going to contact on why we predict AT&T’s cross-bundle discounting will develop after they attain the 30 million threshold (there’s a very attention-grabbing quote from John Stankey within the earnings launch which speaks about homeowners’ economics). We consider that this can put extra stress on cable to complement Verizon’s community with extra CBRS builds with a purpose to stay aggressive with AT&T’s converged bundle value.

Many different analysts have identified AT&T’s double-digit service income declines of their enterprise wireline section (down 11% yr./ yr. and over 4% sequentially). Not like Verizon (the place prices of companies are falling quicker on a proportion foundation than revenues), AT&T must speed up their efforts to scale back entry bills outdoors of their working territory (and in addition allocate sources in territory to switch copper with fiber wherever attainable). Verizon appears effectively on their option to doing this and AT&T ought to copy these performs.

Backside line – AT&T: Ma Bell has the most important executional threat in 2024 with houses handed acceleration and C-Band deployments required. We don’t see how, absent asset gross sales, they may attain their 2.5x leverage ratio goal in 2025. AT&T’s 10-Ok will likely be a should learn for all present traders, notably with respect to deleveraging, OPEB (pension) obligations, and working leases.

T-Cell earnings (outdoors of the shares excellent miss by most analysts) have been very robust. We’re not shocked by the corporate’s efficiency and applaud their “no excuses” mentality to monetary efficiency. Curiously, wholesale revenues are declining quickly at T-Cell (see their detailed working revenue assertion) however that didn’t hold them from posting stellar free money circulate as proven within the following desk:

We’re very shocked by the low capital spend for the quarter however have been comforted by the forecast of $8.6-9.4 billion in capital spending for 2024. This could equate to low teenagers capital spending as a proportion of service revenues and permit T-Cell loads of room for rural enlargement.

Talking of rural initiatives (that are progressing properly due to feedback by Client Group President Jon Freier on the decision), we want to suggest the next concept:

- T-Cell declares as much as $3 billion in rural funding (by a convertible bond) to all BEAD members

- In change for offering this funding, T-Cell would change into the retail gross sales accomplice for every winner (they might use a “retailer inside a retailer” idea)

- Every winner would supply fiber to T-Cell for his or her use at price (or a commercially affordable price)

- T-Cell would obtain a proper of first refusal on the sale of any firm

This is not going to work with sure varieties of members (e.g., an electrical cooperative or a municipality) however would work for a lot of potential bidders. Like Google Fiber’s contest to find out the route of their fiber footprint, we predict Mighty Magenta may tip the scales whereas additionally enabling the 100 Mbps/ 20 Mbps minimal threshold utilizing their huge quantities of licensed spectrum. With the convertible bond strategy and maybe some sales-driven warrants, this may be a intelligent means for T-Cell to win in rural markets with out significant dilution.

Backside line – T-Cell: Glorious “no excuses” quarter with robust money circulate development. Attention-grabbing remark about US Mobile in response to a query about M&A on the finish of the decision that we do not need time to handle on this Temporary.

That’s it for this week. In two weeks, we are going to dive into cable earnings and spherical out our trade observations. Till then, in case you have pals who want to be on the e-mail distribution, please have them ship an electronic mail to [email protected] and we are going to embody them on the record (or they will enroll straight by the web site).

Blissful New Yr, and go Chiefs and Davidson Faculty Basketball!

[ad_2]